Often, corporate boards do not consider how to handle a company bankruptcy until the moment insolvency is looming. As a result, poor, harmful, and even illegal decisions are made by directors unprepared for the hard choices they face. Boards that watch for the signs of financial distress, and act early can cushion the blow, and perhaps avert disaster altogether.

The board of directors is called to a hastily scheduled meeting to discuss an imminent liquidity crisis facing the company. The CFO advises the board that there is insufficient cash in the corporate bank accounts to cover the payroll coming due at the end of the week and there is no further borrowing availability on the company’s revolving credit line.

For the past several months, senior management has negotiated various covenant waivers with its bank group to avoid defaulting under its credit facility. Now, the banks have grown impatient. and are refusing to honor any further draw requests.

The company’s general counsel advises that it is likely the banks next will begin remedial enforcement steps, including freezing accounts with whatever limited cash remains on hand. The board, desperate and with no better alternative, retains bankruptcy counsel. and the company begins to prepare for an urgent Chapter 11 filing.

The future of the company is in question as all parties take sides and prepare for a drawn-out and expensive fight in the bankruptcy court. As the bankruptcy case moves forward. lawsuits regarding how the company reached this point and who is responsible commence.

The above scenario is far too common. How can it be avoided, and what should directors know and do well in advance of their company slipping into a financial crisis? Much has been written about the impact and scope of the “zone of insolvency” and what it means. from a legal perspective, for directors of financially challenged companies. It is important for a board of directors to be advised about the legal ramifications and the types of claims that may be asserted against them in hindsight.

When a company nears insolvency, the board’s focus must shift from solely benefiting investors and shareholders to include other stakeholders, especially creditors.

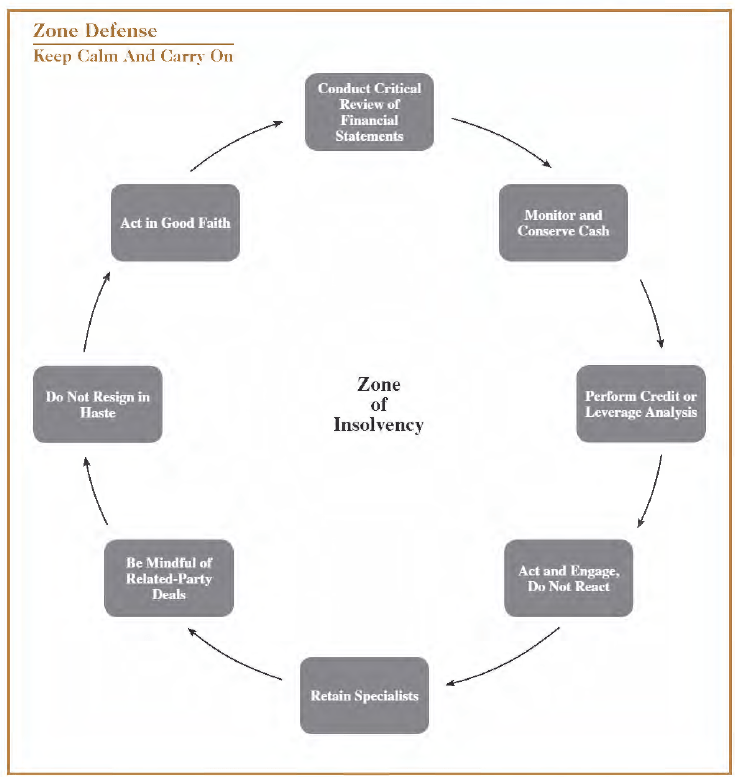

More importantly. though. directors need to understand how, in practical terms. the zone of insolvency impacts their obligations as fiduciaries. What specific steps should directors of a financially challenged company take in the early stages when their company slips into the zone of insolvency? When a company approaches or is in fact insolvent, the focus of the directors must shift from actions that solely benefit the investors and shareholders to how best to preserve and maintain the enterprise for the benefit of all stakeholders. This includes creditors, who effectively become the residual risk bearers as the company’s financial position deteriorates. Directors benefit from the protection of the business judgment rule providing generally that, where directors have behaved reasonably, the decisions they make will not be second-guessed in hindsight. To ensure the continued protection of the business judgment rule in the zone of insolvency. directors must act in good faith. be well informed and must take actions that they genuinely believe to be in the best interests of the enterprise as a whole, rather than simply shareholders and owners. What this means in practice is that the law favors directors who preserve and enhance corporate value for the benefit of all stakeholders. Corporate governance that enhances value will generally satisfy fiduciary duties to both shareholders and creditors.

As such, courts are reluctant to view board members as guarantors of a corporations’ finances. So long as directors pursue proper aims in good faith. the board will generally not be held accountable even to creditors for diminishing corporate value at creditors’ expense.

When a company is in the zone of insolvency. directors should insist on being well informed about the state of affairs of the company. and make careful, reasoned decisions after deliberation on the necessary facts. This includes relying not only on management, but also on appropriate financial and legal experts. Directors are also well advised to appropriately document the process engaged in to make decisions. so that there is evidence of the care and deliberation taken.

Rather than acknowledge the seriousness of the situation and act to address the big issues, many companies treat the challenge as merely a momentary lapse that will self-correct.

There are several actions that the board of a financially distressed entity should consider as its company begins to face impending challenges.

Be realistic and timely. Too many financially challenged firms have difficulty accepting the reality of their situation. We have seen countless examples where companies begin to have cash-flow issues due to operational challenges, over-leverage, macro economic events or some other factors. Rather than acknowledge the seriousness of the situation and act to address the big issues. many companies treat the challenge as merely a momentary lapse that will self-correct (even though they have no specific vision of how that will happen).

Others simply try basic. uncoordinated cash preservation tactics. such as delaying some payables, obvious expense cuts and attempts to accelerate receivable collections or to seek new investments. All of these, of course, are appropriate tools to be employed. However, the board must understand the severity of the situation as it begins to unfold and formulate strategies to address the underlying problems early in the process.

During times of financial distress, increased communication between the board and key members of management is essential. The board must comprehend the capital structure, cash sources and needs, upcoming debt service requirements and underlying issues within and outside of the company’s control that could accelerate an action by creditors. Keen understanding of applicable loan and indenture covenants is critical. Those non-monetary defaults are often the precursor to creditor involvement and potential enforcement remedies.

The primary goal in the early stages of a financial event is for the board to realize and accept the reality of the situation. Begin taking steps on a strategy to address the challenges before a situation deteriorates and creditors begin enforcement actions, or the company reaches a liquidity crisis.

Similarly, it is critical for directors to take account of the situation before the financial erosion is too severe or too much cash has been used. The company may then be significantly impaired in its ability to negotiate with creditors and control the restructuring.

Control cash. A pivotal aspect of any restructuring is understanding the company’s cash flow. It is vital to develop and regularly review realistic cash-flow projections. The board must grasp the company’s liquidity situation, including any contingent liabilities or cash-flow risks. Understanding the flow of funds will inform management and the directors about how much time they have to develop and execute a restructuring plan. Focus immediate attention on times when liquidity may be at its lowest, so the company can immediately implement a coordinated strategy to preserve and maintain its cash.

Your budgeting in a restructuring will be a primary focus for lenders. Generally, they will require distressed borrowers to live within a tightly controlled budget, with certain negotiated variances, and subject to weekly reporting and monitoring. It is crucial to have confidence in your budget projections. and be sure that you actively monitor cash receipts and expenditures to maintain compliance with the lenders· budget and reporting requirements.

Companies may identify “goodwill” as a balance sheet asset, but goodwill is scarce for distressed companies.

Asset valuation and balance sheet. The board must undertake an accurate analysis and estimate of value of the business in the early stages of a restructuring. This analysis includes a critical evaluation of the material assets to assess their true current value.

For example. “goodwill” may be identified as a significant asset on the balance sheet, but goodwill may be hard to realize in a distressed situation.

Similarly. there may be contingent liabilities, such as outstanding litigation, on the balance sheet. These need to be assessed and considered as potential liabilities (at least at some measure of net present value J for any restructuring.)

A primary issue for creditors is valuation. and the company must be able to validate and support its valuation analysis. as the allocation of value is fundamental in any restructuring. In addition. the board should direct the company to evaluate whether there are any valuable assets not subject to lien or pledge. This is also the time for a “collateral perfection” review to understand whether lenders will have any vulnerability.

Creditor leverage analysis. A key strategic consideration for the board of a financially distressed company is to accurately assess the status of each creditor constituency and determine points of lever age and risk for each. This analysis includes assessment of legal and economic risks to creditors and counterparties from a bankruptcy or restructuring, and how best to mitigate those risks. At the end of the day, restructuring is about leverage and opportunity, and this applies to both debtors and creditors.

Act and engage – do not just react. Too many financially challenged companies enter a restructuring without a plan and a long-term strategy. Instead, they simply react to the inevitable crisis of the day, rather than taking steps in a coordinated manner with a long-term focus. We often counsel clients that in any financial restructuring, the most critical step is to formulate the exit plan at the early stages of the proceeding.

Many companies (and, unfortunately. restructuring professionals). fail to realize that actions taken early in a restructuring usually shape the outcome of the ultimate resolution. Directors absolutely must appreciate this as a priority. Immediately take steps to evaluate operational and balance sheet opportunities, and decide what you want to achieve at the end of the restructuring.

Once the board identifies a preliminary restructure strategy, early communication and interaction with key creditors is vital. Creditors are generally more willing to negotiate with distressed companies when they believe that the company is being candid, pre pared and realistic before a crisis strikes.

Generally. when companies reach out to their key creditors too late. or not at all, creditors tend to react with more hostility and aggression. This may put the company in jeopardy and inevitably drives up professional fees.

A key matter for boards to consider is which creditors to include in the preliminary discussions. As a practical matter. it is usually appropriate to start at the top of the capital structure and work down. Make sure the board has a clear and supportable understanding of the enterprise value, and which creditors are (and are not) “in the money” in a potential restructure.

It is essential to identify and retain professionals with relevant experience and credibility. Do not simply default to your usual advisors.

Retain the right professionals. A company in the early stages of financial distress must retain the right professionals. both legal and financial. It is essential for the financially challenged company to identify and retain professionals with relevant experience and credibility with the financial and restructuring community. Do not simply default to the company’s usual advisors. A company in financial distress typically retains a law firm with substantial restructuring experience and. ideally. relevant industry experience. Also seek a financial advisory firm with market credibility to help with the creditor negotiations, restructure modeling and access to capital sources. Consider retaining an interim management firm with professionals who can serve as “chief restructuring officer” or some similar position to lead the turnaround effort. An entire community of legal, financial and interim management professionals exists. It is critical that a financially challenged company retain credible, respected advisors to guide it through the restructuring process. Related-party transactions. It is not uncommon for a corporation in financial distress to turn to previous investors and supporters for help. If this includes shareholders, insiders. or members of the board themselves, the directors should exercise particular care to ensure that there is no conflict of interest that could be later found to taint the decision making process. Even though time may be short, care must be taken to establish appropriate governance procedures, such as establishing a separate committee of the board to analyze any transactions with insiders. Ensure that any such transactions were appropriately evaluated and approved by disinterested parties. Resignation of board members. When a company falls into financial distress (and in particular when a bankruptcy proceeding seems imminent), there is often a temptation for directors to consider resigning from the board. While there is no law that expressly prohibits board members from resigning, it is generally viewed as a derogation of the director’s duties to resign solely to avoid participating in a restructuring. Further. once a company successfully navigates through a Chapter 11 proceeding and institutes a plan of reorganization, such plans often include broad releases of claims in favor of current officers and directors, eliminating any potential future liability for directors. Directors’ and officers’ insurance also generally remains in place during a reorganization proceeding. Crossing the line. When a company is in financial distress, there can be a temptation to cut corners, or look to any potential sources for cash to help bridge the gap. Directors must avoid actions that could expose them directly to personal liability. This can include using funds withheld for payroll taxes to pay corporate expenses. or providing inaccurate or misleading information to the company’s lenders. Board members should avoid scenarios of “deepening insolvency” and assure that appropriate oversight processes are in place to effectively monitor the use of cash and actions of senior management. Directors need to be realistic about any potential bankruptcy situation and respond immediately. When a company enters the zone of insolvency, the board must engage with management to assure that it is fully informed and involved in the decision-making process. The process should focus on steps that lead to what the directors and management reasonably believe will be the best outcome for the enterprise and all of its constituents. Most importantly, directors must be realistic about the situation and respond to it immediately. Once the situation is identified. directors and management should develop a coordinated and comprehensive reorganization strategy to:\- Control cash.

- Assess the value of assets and extent of liabilities.

- Identify creditor leverage points.

- Retain appropriate management and professional advisors.

- Engage early and actively with critical creditors to negotiate and implement an effective reorganization strategy for the company.